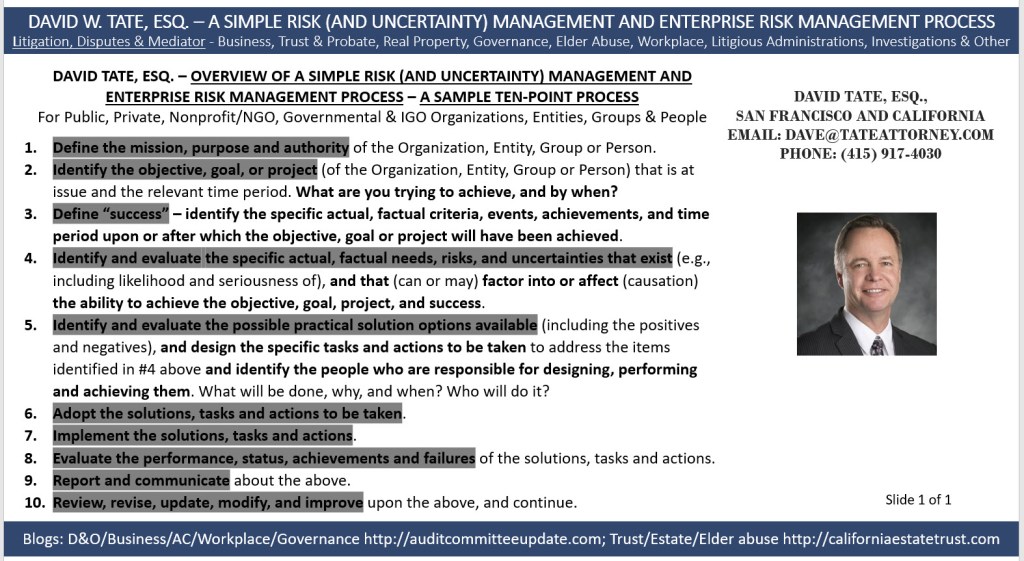

For your ease of reading and reference, the following are the California business judgment rule statutes for:

Corporations – Cal. Corp. Code §309;

Nonprofit public benefit corporations – Cal. Corp. Code §5231;

Nonprofit mutual benefit corporations – Cal. Corp. Code §7231 (and see also §7231.5); and

Nonprofit religious corporations – Cal. Corp. Code §9241 (and see also §9240(c)).

The business judgment rule is state specific – see, for example, Del. Gen. Corp. Law §141 for Delaware corporations, in addition to relevant case law.

Also note that the statutory business judgment rule differs some for corporations, nonprofit public benefit corporations, nonprofit mutual benefit corporations, and nonprofit religious corporations.

Why am I posting this information? Because the business judgment rule is a good rule for people to follow, and to consider, in public company, private business, nonprofit organization, and governmental entity settings and situations. And in this context, when I refer to “people,” I am not referring only to directors, but also to officers, managers and all people throughout the organization. Note: I am not representing that all of these people are legally required to follow the business judgment rule – indeed, the rule is merely a possible defense to liability and possibly relevant to the burden of proof for the people to which it applies and who fact follow the rule – for other people, in the context of this post I am merely suggesting that all people should consider following the rule, or at least keep it in mind as possible guidance in a multitude of public company, private business, nonprofit organization, and governmental entity settings and situations.

Also note that I underlined the provisions below that are underlined (that is, the wording below that is underlined is not underlined in the actual statute).

California Corporations Code Section 309, for corporations:

(a) A director shall perform the duties of a director, including duties as a member of any committee of the board upon which the director may serve, in good faith, in a manner such director believes to be in the best interests of the corporation and its shareholders and with such care, including reasonable inquiry, as an ordinarily prudent person in a like position would use under similar circumstances.

(b) In performing the duties of a director, a director shall be entitled to rely on information, opinions, reports or statements, including financial statements and other financial data, in each case prepared or presented by any of the following:

(1) One or more officers or employees of the corporation whom the director believes to be reliable and competent in the matters presented.

(2) Counsel, independent accountants or other persons as to matters which the director believes to be within such person’s professional or expert competence.

(3) A committee of the board upon which the director does not serve, as to matters within its designated authority, which committee the director believes to merit confidence, so long as, in any such case, the director acts in good faith, after reasonable inquiry when the need therefor is indicated by the circumstances and without knowledge that would cause such reliance to be unwarranted.

(c) A person who performs the duties of a director in accordance with subdivisions (a) and (b) shall have no liability based upon any alleged failure to discharge the person’s obligations as a director. In addition, the liability of a director for monetary damages may be eliminated or limited in a corporation’s articles to the extent provided in paragraph (10) of subdivision (a) of Section 204.

(Amended by Stats. 1987, Ch. 1203, Sec. 2. Effective September 27, 1987.)

California Corporations Code Section 5231, for nonprofit public benefit corporations:

(a) A director shall perform the duties of a director, including duties as a member of any committee of the board upon which the director may serve, in good faith, in a manner that director believes to be in the best interests of the corporation and with such care, including reasonable inquiry, as an ordinarily prudent person in a like position would use under similar circumstances.

(b) In performing the duties of a director, a director shall be entitled to rely on information, opinions, reports or statements, including financial statements and other financial data, in each case prepared or presented by:

(1) One or more officers or employees of the corporation whom the director believes to be reliable and competent in the matters presented;

(2) Counsel, independent accountants or other persons as to matters which the director believes to be within that person’s professional or expert competence; or

(3) A committee upon which the director does not serve that is composed exclusively of any or any combination of directors, persons described in paragraph (1), or persons described in paragraph (2), as to matters within the committee’s designated authority, which committee the director believes to merit confidence, so long as, in any case, the director acts in good faith, after reasonable inquiry when the need therefor is indicated by the circumstances and without knowledge that would cause that reliance to be unwarranted.

(c) Except as provided in Section 5233, a person who performs the duties of a director in accordance with subdivisions (a) and (b) shall have no liability based upon any alleged failure to discharge the person’s obligations as a director, including, without limiting the generality of the foregoing, any actions or omissions which exceed or defeat a public or charitable purpose to which a corporation, or assets held by it, are dedicated.

(Amended by Stats. 2009, Ch. 631, Sec. 14. (AB 1233) Effective January 1, 2010.)

California Corporations Code Section 7231, for nonprofit mutual benefit corporations:

(a) A director shall perform the duties of a director, including duties as a member of any committee of the board upon which the director may serve, in good faith, in a manner such director believes to be in the best interests of the corporation and with such care, including reasonable inquiry, as an ordinarily prudent person in a like position would use under similar circumstances.

(b) In performing the duties of a director, a director shall be entitled to rely on information, opinions, reports or statements, including financial statements and other financial data, in each case prepared or presented by:

(1) One or more officers or employees of the corporation whom the director believes to be reliable and competent in the matters presented;

(2) Counsel, independent accountants or other persons as to matters which the director believes to be within such person’s professional or expert competence; or

(3) A committee upon which the director does not serve that is composed exclusively of any or any combination of directors, persons described in paragraph (1), or persons described in paragraph (2), as to matters within the committee’s designated authority, which committee the director believes to merit confidence, so long as, in any case, the director acts in good faith, after reasonable inquiry when the need therefor is indicated by the circumstances and without knowledge that would cause such reliance to be unwarranted.

(c) A person who performs the duties of a director in accordance with subdivisions (a) and (b) shall have no liability based upon any alleged failure to discharge the person’s obligations as a director, including, without limiting the generality of the foregoing, any actions or omissions which exceed or defeat a public or charitable purpose to which assets held by a corporation are dedicated.

(Amended by Stats. 2009, Ch. 631, Sec. 24. (AB 1233) Effective January 1, 2010.)

See also Cal. Corp. Code §7231.5:

(a) Except as provided in Section 7233 or 7236, there is no monetary liability on the part of, and no cause of action for damages shall arise against, any volunteer director or volunteer executive officer of a nonprofit corporation subject to this part based upon any alleged failure to discharge the person’s duties as a director or officer if the duties are performed in a manner that meets all of the following criteria:

(1) The duties are performed in good faith.

(2) The duties are performed in a manner such director or officer believes to be in the best interests of the corporation.

(3) The duties are performed with such care, including reasonable inquiry, as an ordinarily prudent person in a like position would use under similar circumstances.

(b) “Volunteer” means the rendering of services without compensation. “Compensation” means remuneration whether by way of salary, fee, or other consideration for services rendered. However, the payment of per diem, mileage, or other reimbursement expenses to a director or executive officer does not affect that person’s status as a volunteer within the meaning of this section.

(c) “Executive officer” means the president, vice president, secretary, or treasurer of a corporation or other individual serving in like capacity who assists in establishing the policy of the corporation.

(d) This section shall apply only to trade, professional, and labor organizations incorporated pursuant to this part which operate exclusively for fraternal, educational, and other nonprofit purposes, and under the provisions of Section 501(c) of the United States Internal Revenue Code.

(e) This section shall not be construed to limit the provisions of Section 7231.

(Amended by Stats. 1990, Ch. 107, Sec. 5.)

California Corporations Code Section 9241, for nonprofit religious corporations:

(a) A director shall perform the duties of a director, including duties as a member of any committee of the board upon which the director may serve, in good faith, in a manner such director believes to be in the best interests of the corporation and with such care, including reasonable inquiry, as is appropriate under the circumstances.

(b) In performing the duties of a director, a director shall be entitled to rely on information, opinions, reports, or statements, including financial statements and other financial data, in each case prepared or presented by:

(1) One or more officers or employees of the corporation whom the director believes to be reliable and competent in the matters presented;

(2) Counsel, independent accountants, or other persons as to matters which the director believes to be within that person’s professional or expert competence;

(3) A committee upon which the director does not serve that is composed exclusively of any or any combination of directors, persons described in paragraph (1), or persons described in paragraph (2), as to matters within the committee’s designated authority, which committee the director believes to merit confidence; or

(4) Religious authorities and ministers, priests, rabbis, or other persons whose position or duties in the religious organization the director believes justify reliance and confidence and whom the director believes to be reliable and competent in the matters presented, so long as, in any case, the director acts in good faith, after reasonable inquiry when the need therefor is indicated by the circumstances, and without knowledge that would cause that reliance to be unwarranted.

(c) The provisions of this section, and not Section 9243, shall govern any action or omission of a director in regard to the compensation of directors, as directors or officers, or any loan of money or property to or guaranty of the obligation of any director or officer. No obligation, otherwise valid, shall be voidable merely because directors who benefited by a board resolution to pay such compensation or to make such loan or guaranty participated in making such board resolution.

(d) Except as provided in Section 9243, a person who performs the duties of a director in accordance with subdivisions (a) and (b) shall have no liability based upon any alleged failure to discharge his or her obligations as a director, including, without limiting the generality of the foregoing, any actions or omissions which exceed or defeat any purpose to which the corporation, or assets held by it, may be dedicated.

(Amended by Stats. 2009, Ch. 631, Sec. 33. (AB 1233) Effective January 1, 2010.)

See also Cal. Corp. Code §9240(c):

(c) A director, in making a good faith determination, may consider what the director believes to be:

(1) The religious purposes of the corporation; and

(2) Applicable religious tenets, canons, laws, policies, and authority.

(Amended by Stats. 1987, Ch. 923, Sec. 1.4. Operative January 1, 1988, by Sec. 103 of Ch. 923.)

—————————————————————

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this website. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only.

I am also the Chair of the Business Law Section of the Bar Association of San Francisco.

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrations http://californiaestatetrust.com; Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance, responsibilities and rights, compliance, investigations, and risk management http://auditcommitteeupdate.com

The following are copies of the tables of contents of three of the more formal materials that I have written over the years about accounting/auditing, audit committees, and related legal topics – Accounting and Its Legal Implications was my first formal effort, which resulted in a published book that had more of an accounting and auditing focus; Chapter 5A, Audit Committee Functions and Responsibilities, for the California Continuing Education of the Bar has a more legal focus; and the most recent Tate’s Excellent Audit Committee Guide (February 2017) also has a more legal focus:

Accounting and Its Legal Implications

Chapter 5A, Audit Committee Functions and Responsibilities, CEB Advising and Defending Corporate Directors and Officers

Tate’s Excellent Audit Committee Guide

The following are other summary materials that you might find useful:

From a prior blog post which you can find at https://wp.me/p75iWX-dk if the below scan is too difficult to read:

* * * * *

{kind=link}