This blog primarily discusses litigation and disputes; directors, officers, boards and committees including audit and governance; authorities, responsibilities and rights; liability and compliance with laws; governance and leadership; risk management processes; the workplace; communications and optics; evidence and trials; and mediation, dispute resolution and mediator services. David Tate, Esq., California – Email: dave@tateattorney.com – see also http://californiaestatetrust.com – a blog discussing trust, estate, elder, conservatorship, power of attorney, fiduciary, beneficiary and probate court litigation and contentious administrations

I am a founding member of the San Francisco Chapter of the Private Directors Association (PDA). The San Francisco Chapter was formed in 2020 during COVID. The Chapter is humming along and has over 100 members.

The Private Directors Association has Chapters across the United States, and also two additional Chapters in Southern California.

Each Chapter presents webinars on topics of interest and relevance to private company and organization directors. There are opportunities for webinar sponsors, speakers and panels. Upcoming webinars and events are advertised and promoted to all members and Chapters, not just to the local Chapter.

There are also Chapter sponsorship opportunities which provide additional benefits and exposure for the sponsor.

For additional information, if you would like, you can reach out to me at dave@tateattorney.com. I have also linked below the current webinar sponsor/speaker packet, a brochure for the San Francisco Chapter, and a brochure for National PDA.

Immediately below in the following order you will find links for the current webinar sponsor/speaker packet, a brochure for the San Francisco PDA Chapter, and a brochure for National PDA.

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

I have provided below a link to California SB 260 – Climate Corporate Accountability Act – introduced January 26, 2021. I try to comment about legislation only when it fits within the scope of my topic areas or the topic areas of other people with whom I am working. It is a given that businesses will be seeing an increasing number of climate-related disclosure and compliance laws, regulations and rules, in addition to the increased stakeholder, community and consumer interests in those topics and in ESG + Sustainability + Climate Action.

But these topics also raise a lot of questions that need to be answered. For example, reading SB 260, which is a short piece of legislation, I have a comment or question about the majority of the sentences in the legislation – such as “please define that . . . ” or “what does that mean . . .” or “what is required for compliance . . “ or “after you first define the specific problem and goal to be achieved, and why, what is the anticipated ROI on that or this . . . “?

I presume that at many businesses, audit committees will be tasked with oversight. And finally, from a 10,000-foot view, my approach to drafting the legislation and to compliance would be a risk management processes approach (see slide picture below) with a view toward defining the very specific problem and issue, defining the specific goal and success, the reasonable options that are available, and the pros and cons for each and ROI. Additionally, assuming, arguendo, that California has legal authority to draft its own laws on this and to regulate in this manner each “publicly traded domestic or publicly traded foreign corporation with annual revenues in excess of one billion dollars ($1,000,000,000) that does business in California,” has the Legislature addressed whether these issues will be addressed at a national level with the Biden administration?

Again, the proposed legislation is a short piece. And there will be a lot more to follow in California, and nationally, and internationally. See the link to the legislation below.

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes, Mediator & Governance: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrationshttp://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, ESG + sustainability, and risk managementhttp://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, Boards and Committees, Officers, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, compliance, ESG, sustainability, etc.; and advising audit committees, governance committees, officers, directors, and boards.

Mediator Services and Dispute Resolution

Trust, estate, elder and elder abuse, conservatorship, power of attorney, and other probate court cases.

Business: breach of contract.

Business: owner, founder, partner, shareholder, investor, board and committee, officer, and governance disputes.

Employment and workplace, discrimination, wrongful termination, and harassment.

ESG criteria refers to an organization’s environmental, social and governance policies, practices and processes, some of which depend upon whether the organization is a public corporation or business, private corporation or business, nonprofit, not for profit or NGO, governmental organization or entity, or a hybrid or mixed organization or entity. ESG criteria will also vary depending on the size of the organization or entity, its industry, and whether it primarily provides a service, a product or manufacturing, or a combination of both.

The following criteria can be used for reference; indeed, however, whereas applicable criteria have been set in some circumstances or for some situations, applicable criteria otherwise often remain in a state of change, discretion, suggestion or proposal, and choice. The various services that evaluate and rate ESG also each individually decide which criteria they will use. Indeed, the below listed possible criteria are intended to be fairly encompassing so as to promote thought and consideration, but are not necessarily in the whole a list of required criteria. Each organization and entity must evaluate its own requirements and circumstances.

Environmental criteria broadly refer to some or all of the following:

Resource materials and energy evaluation, selection, use, and discharge, management and conservation;

Environmental risks and management;

Waste;

Emissions;

Pollution;

Hazardous and toxic wastes and emissions;

Ownership and management of contaminated materials and land;

Treatment of animals; and

Compliance with laws and regulations.

Depending on the processes that are being used sometimes the environmental component of ESG can be the more clear-cut or direct component to identify and measure.

Social criteria broadly refer to some or all of the following:

The organization’s or entity’s internal and external relationships, values and culture and its adherence to and enforcement of values with employees and independent contractors in the workplace and work environment;

Its working relationship employees, independent contractors and in the workplace, with customers, with suppliers, in the community, and with other stakeholders;

Human capital, as it has been called – I don’t particularly like the term “human capital” as to me it sounds a bit faceless or depersonalized – instead I prefer something such as simply the category “People”;

Health and safety;

Well-being;

Diversity;

Opportunities provided, inclusiveness and equality, training, mentorship, advancement and advancement opportunities;

Talent acquisition and retention;

Social engagement and active involvement;

Discrimination;

Organizational openness and communications;

Organizational trust, integrity and reputation; and

Compliance with laws and regulations.

I view the social criteria component of ESG as being the more currently challenging component because of the very large numbers of criteria that people can argue are or should be included, and its sometimes difficulty of measurement or more subjective nature.

Governance criteria broadly refer to some or all of the following:

The organization or entity overall, and to its leaders and their actions and leadership including such criteria as:

Board and management roles, makeup, structure, policies, processes and practices;

Decision making;

Accounting methods and related transparency;

Shareholder engagement and shareholder rights;

Avoidance of unlawful practices, and legally or ethically questionable business practices;

Strong, transparent and enforced governance policies and practices;

Codes of conduct and ethics, and enforcement;

Board, executive officer and senior management diversity;

Measurement of corporate and organization performance;

Corporate and organization values, trust, integrity, and reputation;

Board oversight;

Accountability for actions;

Oversight of internal controls;

Oversight of compliance with laws and regulations;

Compensation;

Avoidance of unlawful conflicts of interest;

Information disclosure;

Corporate and organization sustainability;

Oversight of environmental, social and governance criteria;

The organization’s use of information and private information, and information and cyber security;

Protection of the organization’s assets including intellectual property;

Officer, director, and management openness to appropriate challenges, disagreement, and criticism, and the manner and processes for learning about, addressing, evaluating and debating, decision making, and resolving those ongoing occurrences and situations; and

Board and director structure, agenda setting, demeanor, meeting processes, independence, and adherence to prudent business judgment and diligent, active and proactive business judgment rule practices.

Whereas the above list of possible governance criteria might suggest that the governance component of ESG is more well-defined, I view the governance criteria as currently being perhaps the more challenging component of ESG because a large number of possible criteria can be identified but in practice the criteria that are recognized as being accepted tend to be less numerous, and as a group governance criteria still tend to be more vague, undefined and less agreed upon, and identification, evaluation and measurement of governance criteria also tend to vary more from organization and entity to organization and entity.

Best to you. David Tate, Esq. (and inactive CPA)

——————————————————————–

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes, Mediator & Governance: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrationshttp://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, ESG + sustainability, and risk managementhttp://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, Boards and Committees, Officers, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, compliance, ESG, sustainability, etc.; and advising audit committees, governance committees, officers, directors, and boards.

Mediator Services and Dispute Resolution

Trust, estate, elder and elder abuse, conservatorship, power of attorney, and other probate court cases.

Business: breach of contract.

Business: owner, founder, partner, shareholder, investor, board and committee, officer, and governance disputes.

Employment and workplace, discrimination, wrongful termination, and harassment.

I have provided below a link to a pdf of a new paper (September 2020) that is written as “the result of a collaboration between the PRI and the Climate Risk Initiative at UC Berkeley School of Law’s Center for Law, Energy & the Environment.” The UNEP Finance Initiative also appears to be an author or sponsor.

The paper and its recommendations are not law. However, the paper is potentially (i.e., appears to be) more than simply discussion when you view the Acknowledgements (page 4) and the Forwards (pages 5-7).

The paper contains 40 recommendations in 7 categories which encourage California to enact legislation and/or regulations that require ESG standards or processes and disclosures for the listed entities and organizations.

I will not be spending much time on this paper for the reason that as a general rule I don’t spend much time on discussion papers that are not proposed or actual legislation, regulations or rules. However, I am mentioning this paper because I am presuming that it was written with at least some buy-in from other people who have the authority to make some or all of the provisions enforceable by law. And I note that at page 26, under the heading “Challenges” with respect to ESG integration, the paper notes “A lack of consistent, comparable, robust, and widely available ESG data . . . ,” and the paper also does contain the 40 specific recommendations many of which relate to statutes (law) or regulations (also law).

One additional comment about the paper and ESG standards, while the paper in part discusses legislation to require and mandate that certain non-governmental businesses implement certain ESG standards and reporting or disclosure, the paper also discussed or provides ESG recommendations for governmental organizations in California – for which I presume that ESG standards and reporting (i.e., standards and reporting for governmental entities and organizations) could be ordered or required immediately or relatively easily right now – thus, one approach would be for governmental entities and organizations to lead the way by example.

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes, Mediator & Governance: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrationshttp://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, ESG, and risk managementhttp://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, etc.; and advising audit committees, governance committees, officers, directors, and boards.

At the bottom of this post I have included a link to an article in Forbes that I find worthwhile for beginning the steps toward your design and implementation of ESG.

One of the current difficulties with starting to design and implement ESG for your organization is that there continues to be no single definition or list of criteria for exactly what ESG is, and, thus, what is included in ESG. Perhaps related, but really a different issue, is that there is no agreed upon standard or process for how to audit or even evaluate ESG from one organization to the next. For example, the following are some of the various standards that have been developed for ESG standards and evaluating ESG, and which contain their various respective criteria and components including for example SASB (Sustainability Accounting Standards Board), GRI (Global Reporting Initiative), UN SDGs (UN Sustainable Development Goals), MSCI, ISS ESG, and Sustainalytics (Morningstar), to name some.

However, stepping back a few steps from the above paragraph, it can also be argued that the lack of one or two definitive standards might also be a benefit for the majority of organizations that want to start designing and implementing their ESG. I say that because while a significant focus has been directed toward ESG in public companies and possible required regulations, all of which takes time and has taken time and regulations and legal requirements whatever they are and whatever they might become will in any event be a progression of starts and stops, the fact is that the great, great majority of organizations are nonpublic, nonprofit and governmental to which legal requirements for public companies will not apply, or only might at some point become relevant but typically not in a legal required sense.

There is in fact no obstruction to any organization, whether public, nonpublic, nonprofit or governmental, designing, implementing, and even reporting ESG. That having been said, however, depending on the type of organization “reporting” and what the organization says or represents about its ESG will require consideration from a legal perspective, but that also is true about everything that the organization reports or says or represents about its operations, policies, conduct, governance, etc.

Looking more at specific design and implementation of ESG, the following is a link to an article in Forbes that I find worthwhile for beginning the steps toward your design and implementation of ESG: “How to Operationalize ESG” https://www.forbes.com/sites/betsyatkins/2020/05/08/how-to-operationalize-esg/?sh=601883294835. One of the points is that the organization has the ability, and even for public companies at least in part the ability, to design and implement its own ESG and can start small, limited or specifically focused and can then grow from there, keeping in mind, of course, that what the organization reports or says or represents about its ESG will require consideration from a legal perspective.

Best to you. David Tate, Esq.

——————————————————————–

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes, Mediator & Governance: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrations http://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, and risk management http://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, etc.; and advising audit committees, governance committees, officers, directors, and boards.

I have become a member of the Private Directors Association and the San Francisco Chapter in which I am participating. The following is a link to the webpage for the San Francisco Chapter: https://www.privatedirectorsassociation.org/chapters/san-francisco-chapter/, and you can view the organization as a whole at http://www.privatedirectorsassociation.org. As you might be aware, the great majority of businesses and organizations are private (i.e., non-public entities). The PDA is a very active organization nationally and locally with many multiple state chapters, and with new chapters in progress – in my view you should take a look.

Best to you. David Tate, Esq.

——————————————————————–

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes, Mediator & Governance: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrations http://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, and risk management http://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, etc.; and advising audit committees, governance committees, officers, directors, and boards.

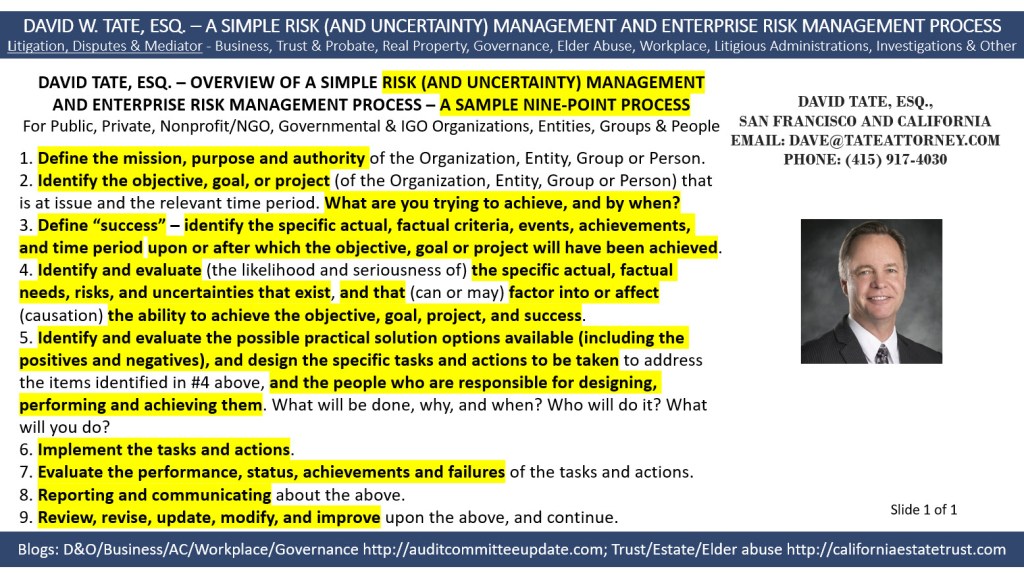

Below I have provided a link to a short video on youtube in which I discuss a simple nine point risk management and ERM process. Please do feel free to also pass this information to anyone else who might be interested.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing as a lawyer in California only

———————————————————————-

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes & Mediator: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs:

Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrations http://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, and risk management http://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, etc.; and advising audit committees, governance committees, officers, directors, and boards.

David W. Tate, Esq., San Francisco and California – dave@tateattorney.com

You may have heard that the U.S. Department of Justice, Criminal Division has updated its Evaluation of Corporate Compliance Programs (June 2020). I have provided below a link to the updated guidance. The changes can be and are important.

The updated guidance will be discussed in many legal articles and blog posts. And I have not had the time to digest all of the changes. However, for example, below I have provided a snapshot of a paragraph that has been revised and expanded in the Introduction section, and also a snapshot of the revised three fundamental questions (note the revisions to number 2 requiring that the program be adequately resourced and empowered to function effectively). The third fundamental question also still remains challenging, i.e., “Does the corporation’s compliance program work” in practice, and what do you have to do to be able to make the determination that it does “work”?

Best to you, Dave Tate, Esq. (San Francisco and California) – dave@tateattorney.com

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only.

I am also the Chair of the Business Law Section of the Bar Association of San Francisco.

Blogs

Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrations http://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, and risk management http://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, etc.; and advising audit committees, governance committees, officers, directors, and boards.

Mediator Services and Conflict Resolution

Mediation and Conflict Resolution Hexagon Matrix to Help Achieve Resolution and Settlement – Dave Tate, Esq.

{kind=link}