This blog primarily discusses litigation and disputes; directors, officers, boards and committees including audit and governance; authorities, responsibilities and rights; liability and compliance with laws; governance and leadership; risk management processes; the workplace; communications and optics; evidence and trials; and mediation, dispute resolution and mediator services. David Tate, Esq., California – Email: dave@tateattorney.com – see also http://californiaestatetrust.com – a blog discussing trust, estate, elder, conservatorship, power of attorney, fiduciary, beneficiary and probate court litigation and contentious administrations

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

I am forwarding below a link to an article by Dan Ballesteros, discussing “A new frontier has arrived for Americans with Disabilities Act (ADA) compliance lawsuits: lawsuits for non-compliant websites.” Dan’s discussion is useful, and is fairly detailed. Impacted websites must be ADA compliant. See also Dan’s reference to the California Consumer Privacy Protection Act (CCPA) and privacy policy accessibility requirements. Here is the link to the article: https://www.hogefenton.com/news-events/ada-lawsuits-websites-website-compliant-2/

I have pasted below and I have attached a pdf of a paper that is written by Amanda North who is the Founder and CEO of Plan C Advisors. Plan C Advisors helps businesses plan for and implement current and upcoming climate change requirements. The paper is a helpful read that contains five action points that help to point businesses in the right direction. If the links in Amanda’s paper that I have copied and pasted below don’t work, I believe that the links in the pdf will. Enjoy the paper, and contact Ms. North (Amanda) if you would like to explore how Plan C Advisors can help you.

You will find the pdf link immediately below, and I have copied and pasted Amanda’s paper below the link:

Five Steps to Prepare for 2021 – The Year of (Climate) Change

By Amanda North, Plan C Advisors Founder and CEO

After mounting pressure from stakeholders and growing evidence of climate change impacts, the stars have aligned — the Biden Administration is making climate a top priority, leading asset managers are requiring portfolio companies treat climate as a material issue, and companies around the world are pledging bolder climate actions. According to a recent Pew Research poll, citizens in Europe and around the world believe climate is the crisis of ongoing and greatest importance facing our shared planet. By all measures, 2021 is shaping up to be a year of accelerating climate action in the US and around the world.

If business leaders are not already in deep planning mode, they should get ready — fast. Members of the Plan C Advisors team suggest 5 steps to get started:

#1 Plan for Climate Risk Across the Entire Organization

COVID-19 should be a wake-up call to business leaders thinking about climate. Like the pandemic, the early warning signs of climate impacts were largely ignored and climate has now reached crisis stature. Plan C Advisors counsels company leaders to map climate-related organizational risks and opportunities across the entirety of your business and develop enterprise-wide action plans. Jupiter Intelligence, a Plan C Advisors partner, helps companies predict the physical impacts of climate and develop risk mitigation strategies by utilizing new generations of sophisticated, AI-based, software. Potential impacts to reputation, brand strength and customer loyalty also must be considered recommends Jennifer Swint. Additionally, because of climate change, some companies may need to reconsider the fundamentals of their business as Simon Todd counsels clients in the energy sector who are faced with the fundamental challenge of transitioning their traditional products, services and operations.

#2 Leverage Climate Demands to Create Company Value

Organizations that understand their Purpose, have a culture of fearless innovation, and act decisively can find opportunities to evolve their products and services and launch new businesses in response to climate challenges. Pivoting company leadership to look at climate as a business opportunity will lead to more innovation and ingenuity that will be good for your bottom line as well as the planet. Lisa Bougie leverages her career as an executive in the apparel sector, one of the industries under greatest duress from climate factors, to help clients consider creative approaches to climate impacts. In the apparel sector this includes new business models such as renting vs buying clothing, use of new planet-friendly materials and upcycling. Celso White draws on his many years as an executive with global food and beverage companies to help clients rethink their supply chain operations to increase efficiencies and improve their climate footprint. And Chris Miller, Plan C Advisor and partner at AJW a leading government affairs consultancy, advises business leaders to proactively advance policies on climate that align with their business strategies.

#3 Develop Ongoing, Bi-directional, Communications with Stakeholders

In this era of transparency, the full range of company stakeholders—employees, customers, partners, and investors–all demand knowledge of corporate climate actions. They no longer are satisfied with platitudes, but with the kind of concrete examples of climate action that Silverline Communications uses as the basis for communications on behalf of its clients. Importantly, audiences want to be engaged on the topic of climate, not merely spoken to. Collaboration with affected communities, industry groups, NGOs as well as governmental entities across geographic regions is a requirement for effective climate action. Climate Justice expert Bee Hui Yeh, emphasizes that all voices must be included in order to drive climate solutions that are healthy, just and sustainable for all.

#4 Disclose, Even with Imperfect Information

Formal disclosures are playing an increasingly important role in climate communications. Plan C Advisors Partner GAA says even if you have imperfect information, and even if not all the news is positive, it is critical that you disclose your climate impact and exposure using at least one of the myriad standards and frameworks now available for that purpose. For instance, if investors are a critical audience for your organization, using the SASB disclosing standards would be a good first step. Disclosures have been complex, changing and burdensome for businesses, but there are positive signs that this is changing as the value of disclosing receives more mainstream acceptance—and quite likely soon will be mandated in the US as it is in many parts of the world.

#5 Engage Your Board

BlackRock and other major asset managers are increasingly vocal about holding board directors accountable for making progress on sustainability-related goals, including climate. D’Anne Hurd, recommends that board directors play a vital role in setting the tone and guiding the adoption of climate strategies. Tracy Edkins advises boards to engage more directly with management to catalyze the organizational transformation needed to drive climate action across the enterprise, including aligning language, incentives and compensation–not a small task particularly when working with a sprawling, global and fast-growing organization as she has in her role as chief people officer in the tech sector.

Call to action—Readiness Assessment

Fortunately, all signs point to the pace of climate awareness and action rapidly accelerating in 2021, particularly as the Biden Administration takes office. This is the year for all business leaders to ensure they have a plan in place to address climate throughout their organizations. Silverline Communications and Plan C Advisors can get you started with an initial diagnostic to assess organizational readiness and recommend priority next steps. Please reach out to Amanda North at anorth@plancadvisors.com to learn more.

Best to you. David Tate, Esq. (and inactive CPA)

——————————————————————–

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes, Mediator & Governance: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrationshttp://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, ESG + sustainability, and risk managementhttp://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, Boards and Committees, Officers, Authority, Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, compliance, ESG, sustainability, etc.; and advising audit committees, governance committees, officers, directors, and boards.

Mediator Services and Dispute Resolution

Trust, estate, elder and elder abuse, conservatorship, power of attorney, and other probate court cases.

Business: breach of contract.

Business: owner, founder, partner, shareholder, investor, board and committee, officer, and governance disputes.

Employment and workplace, discrimination, wrongful termination, and harassment.

I have provided below a link to California SB 260 – Climate Corporate Accountability Act – introduced January 26, 2021. I try to comment about legislation only when it fits within the scope of my topic areas or the topic areas of other people with whom I am working. It is a given that businesses will be seeing an increasing number of climate-related disclosure and compliance laws, regulations and rules, in addition to the increased stakeholder, community and consumer interests in those topics and in ESG + Sustainability + Climate Action.

But these topics also raise a lot of questions that need to be answered. For example, reading SB 260, which is a short piece of legislation, I have a comment or question about the majority of the sentences in the legislation – such as “please define that . . . ” or “what does that mean . . .” or “what is required for compliance . . “ or “after you first define the specific problem and goal to be achieved, and why, what is the anticipated ROI on that or this . . . “?

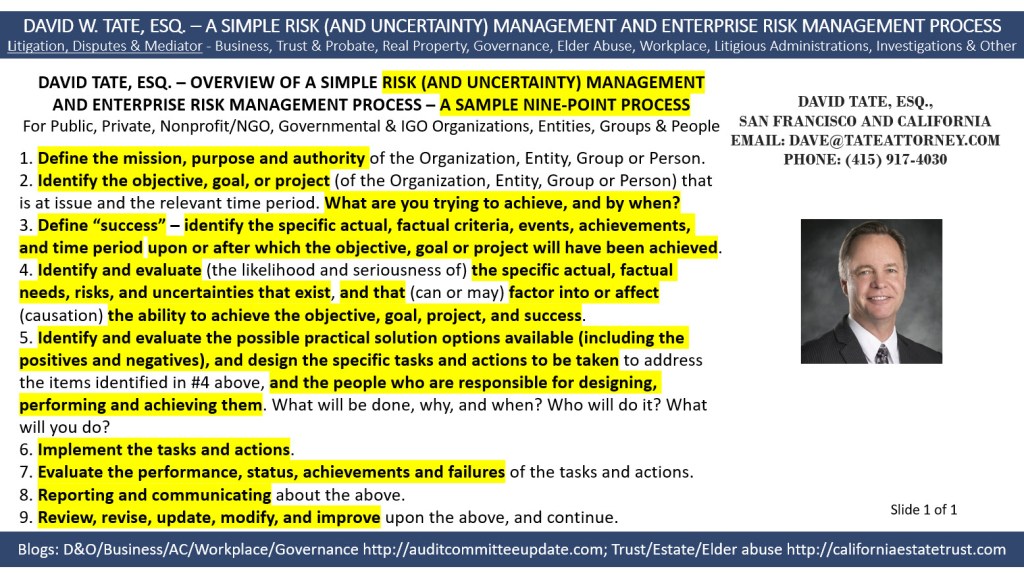

I presume that at many businesses, audit committees will be tasked with oversight. And finally, from a 10,000-foot view, my approach to drafting the legislation and to compliance would be a risk management processes approach (see slide picture below) with a view toward defining the very specific problem and issue, defining the specific goal and success, the reasonable options that are available, and the pros and cons for each and ROI. Additionally, assuming, arguendo, that California has legal authority to draft its own laws on this and to regulate in this manner each “publicly traded domestic or publicly traded foreign corporation with annual revenues in excess of one billion dollars ($1,000,000,000) that does business in California,” has the Legislature addressed whether these issues will be addressed at a national level with the Biden administration?

Again, the proposed legislation is a short piece. And there will be a lot more to follow in California, and nationally, and internationally. See the link to the legislation below.

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes, Mediator & Governance: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrationshttp://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, ESG + sustainability, and risk managementhttp://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, Boards and Committees, Officers, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, compliance, ESG, sustainability, etc.; and advising audit committees, governance committees, officers, directors, and boards.

Mediator Services and Dispute Resolution

Trust, estate, elder and elder abuse, conservatorship, power of attorney, and other probate court cases.

Business: breach of contract.

Business: owner, founder, partner, shareholder, investor, board and committee, officer, and governance disputes.

Employment and workplace, discrimination, wrongful termination, and harassment.

ESG criteria refers to an organization’s environmental, social and governance policies, practices and processes, some of which depend upon whether the organization is a public corporation or business, private corporation or business, nonprofit, not for profit or NGO, governmental organization or entity, or a hybrid or mixed organization or entity. ESG criteria will also vary depending on the size of the organization or entity, its industry, and whether it primarily provides a service, a product or manufacturing, or a combination of both.

The following criteria can be used for reference; indeed, however, whereas applicable criteria have been set in some circumstances or for some situations, applicable criteria otherwise often remain in a state of change, discretion, suggestion or proposal, and choice. The various services that evaluate and rate ESG also each individually decide which criteria they will use. Indeed, the below listed possible criteria are intended to be fairly encompassing so as to promote thought and consideration, but are not necessarily in the whole a list of required criteria. Each organization and entity must evaluate its own requirements and circumstances.

Environmental criteria broadly refer to some or all of the following:

Resource materials and energy evaluation, selection, use, and discharge, management and conservation;

Environmental risks and management;

Waste;

Emissions;

Pollution;

Hazardous and toxic wastes and emissions;

Ownership and management of contaminated materials and land;

Treatment of animals; and

Compliance with laws and regulations.

Depending on the processes that are being used sometimes the environmental component of ESG can be the more clear-cut or direct component to identify and measure.

Social criteria broadly refer to some or all of the following:

The organization’s or entity’s internal and external relationships, values and culture and its adherence to and enforcement of values with employees and independent contractors in the workplace and work environment;

Its working relationship employees, independent contractors and in the workplace, with customers, with suppliers, in the community, and with other stakeholders;

Human capital, as it has been called – I don’t particularly like the term “human capital” as to me it sounds a bit faceless or depersonalized – instead I prefer something such as simply the category “People”;

Health and safety;

Well-being;

Diversity;

Opportunities provided, inclusiveness and equality, training, mentorship, advancement and advancement opportunities;

Talent acquisition and retention;

Social engagement and active involvement;

Discrimination;

Organizational openness and communications;

Organizational trust, integrity and reputation; and

Compliance with laws and regulations.

I view the social criteria component of ESG as being the more currently challenging component because of the very large numbers of criteria that people can argue are or should be included, and its sometimes difficulty of measurement or more subjective nature.

Governance criteria broadly refer to some or all of the following:

The organization or entity overall, and to its leaders and their actions and leadership including such criteria as:

Board and management roles, makeup, structure, policies, processes and practices;

Decision making;

Accounting methods and related transparency;

Shareholder engagement and shareholder rights;

Avoidance of unlawful practices, and legally or ethically questionable business practices;

Strong, transparent and enforced governance policies and practices;

Codes of conduct and ethics, and enforcement;

Board, executive officer and senior management diversity;

Measurement of corporate and organization performance;

Corporate and organization values, trust, integrity, and reputation;

Board oversight;

Accountability for actions;

Oversight of internal controls;

Oversight of compliance with laws and regulations;

Compensation;

Avoidance of unlawful conflicts of interest;

Information disclosure;

Corporate and organization sustainability;

Oversight of environmental, social and governance criteria;

The organization’s use of information and private information, and information and cyber security;

Protection of the organization’s assets including intellectual property;

Officer, director, and management openness to appropriate challenges, disagreement, and criticism, and the manner and processes for learning about, addressing, evaluating and debating, decision making, and resolving those ongoing occurrences and situations; and

Board and director structure, agenda setting, demeanor, meeting processes, independence, and adherence to prudent business judgment and diligent, active and proactive business judgment rule practices.

Whereas the above list of possible governance criteria might suggest that the governance component of ESG is more well-defined, I view the governance criteria as currently being perhaps the more challenging component of ESG because a large number of possible criteria can be identified but in practice the criteria that are recognized as being accepted tend to be less numerous, and as a group governance criteria still tend to be more vague, undefined and less agreed upon, and identification, evaluation and measurement of governance criteria also tend to vary more from organization and entity to organization and entity.

Best to you. David Tate, Esq. (and inactive CPA)

——————————————————————–

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes, Mediator & Governance: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrationshttp://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, ESG + sustainability, and risk managementhttp://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, Boards and Committees, Officers, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, compliance, ESG, sustainability, etc.; and advising audit committees, governance committees, officers, directors, and boards.

Mediator Services and Dispute Resolution

Trust, estate, elder and elder abuse, conservatorship, power of attorney, and other probate court cases.

Business: breach of contract.

Business: owner, founder, partner, shareholder, investor, board and committee, officer, and governance disputes.

Employment and workplace, discrimination, wrongful termination, and harassment.

The following is a link to an article by Hedley Lawson of Aligned Growth Partners discussing new SEC amendments to Regulation S-K and requiring disclosure of human capital resources measures and objectives that the company focuses on in managing its business:

I particularly note (and I have pasted below) the discussion wherein Hedley lists broad categories that should receive consideration while also recognizing that “each company will need to evaluate its own particular circumstances to identify its human capital resources and determine their materiality to an understanding of its business.” The categories are also helpful for consideration in the context of the employer and workforce component of the “S” (social) criteria in ESG (environmental, social and governance). The following are the broad categories that are listed in the article:

CATEGORY POTENTIAL TOPICS Workforce governance · Board or committee oversight of human capital strategy · Role and expectations of the Chief Human Resources Officer · Legal and ethical compliance Workforce composition · Agile and transformational talent acquisition and recruiting · Meaningful, measurable, and sustainable diversity, equity, and inclusion · Experience and education of workforce Workforce stability · Voluntary and involuntary turnover analytics · Actionable succession planning and employee promotability · Meaningful employee satisfaction surveys Workforce skills and development · Professional and personal development opportunities Workforce culture · Employee engagement · Work-life initiatives · Employee health, safety, and well-being programs · Employee recognition programs Workforce compensation (in the absence of a Compensation Committee) · Gender, racial, and generational pay equality · Incentives and cash and non-cash benefits · Targeted market compensation data and analysis

More to follow on these topics including human capital and ESG + Sustainability.

Best to you. David Tate, Esq.

——————————————————————–

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes, Mediator & Governance: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrationshttp://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, ESG + sustainability, and risk managementhttp://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, Boards and Committees, Officers, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, compliance, ESG, sustainability, etc.; and advising audit committees, governance committees, officers, directors, and boards.

Mediator Services and Dispute Resolution

Trust, estate, elder and elder abuse, conservatorship, power of attorney, and other probate court cases.

Business: breach of contract.

Business: owner, founder, partner, shareholder, investor, board and committee, officer, and governance disputes.

Employment and workplace, discrimination, wrongful termination, and harassment.

I have provided below a link to a pdf of a new paper (September 2020) that is written as “the result of a collaboration between the PRI and the Climate Risk Initiative at UC Berkeley School of Law’s Center for Law, Energy & the Environment.” The UNEP Finance Initiative also appears to be an author or sponsor.

The paper and its recommendations are not law. However, the paper is potentially (i.e., appears to be) more than simply discussion when you view the Acknowledgements (page 4) and the Forwards (pages 5-7).

The paper contains 40 recommendations in 7 categories which encourage California to enact legislation and/or regulations that require ESG standards or processes and disclosures for the listed entities and organizations.

I will not be spending much time on this paper for the reason that as a general rule I don’t spend much time on discussion papers that are not proposed or actual legislation, regulations or rules. However, I am mentioning this paper because I am presuming that it was written with at least some buy-in from other people who have the authority to make some or all of the provisions enforceable by law. And I note that at page 26, under the heading “Challenges” with respect to ESG integration, the paper notes “A lack of consistent, comparable, robust, and widely available ESG data . . . ,” and the paper also does contain the 40 specific recommendations many of which relate to statutes (law) or regulations (also law).

One additional comment about the paper and ESG standards, while the paper in part discusses legislation to require and mandate that certain non-governmental businesses implement certain ESG standards and reporting or disclosure, the paper also discussed or provides ESG recommendations for governmental organizations in California – for which I presume that ESG standards and reporting (i.e., standards and reporting for governmental entities and organizations) could be ordered or required immediately or relatively easily right now – thus, one approach would be for governmental entities and organizations to lead the way by example.

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes, Mediator & Governance: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrationshttp://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, ESG, and risk managementhttp://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, etc.; and advising audit committees, governance committees, officers, directors, and boards.

The following is a link to a pdf of Measuring Stakeholder Capitalism: Towards Common Metrics and Consistent Reporting of Sustainable Value Creation (a 96 page paper):

The paper, which was published in September 2020, is a project of the International Business Council (IBC) of the World Economic Form (WEF) in collaboration with Deloitte, EY, KPMG and PwC. I believe that this is the first time that the Big 4 have gotten together in an effort to develop ESG and sustainability standards.

The paper defines the finished project as follows: “This work defines a core set of “stakeholder Capitalism Metrics” (SCM) and disclosures that can be used by IBC members to align their mainstream reporting on performance against environmental, social and governance (ESG) indicators and track their contributions towards the SDGs [UN Sustainable Development Goals] on a consistent basis.”

The paper and its ESG metrics are based on four pillars:

Pillar 1: Principles of Governance;

Pillar 2: Planet;

Pillar 3: People; and

Pillar 4: Prosperity.

This paper is a good initial effort to define measurable standards and metrics. In light of the authors and contributors this paper and its further related amendments, tweaks, and discussions will become a direct standard for IBC members, and some parts of it will become indirect or voluntary standards for some other organizations.

Many provisions in the paper are heavily focused on GRI (Global Reporting Initiative) standards. Thus, for example, the paper does not focus on SASB (Sustainability Accounting Standards Board) standards. You might also be aware that the SASB and the IIRC (International Integrated Reporting Council) announced on November 25, their intent to merge into a unified organization “in major step towards simplifying the corporate reporting system.” A lot of significant developments and changes are occurring in the ESG and sustainability areas.

As the IBC/Big-4 paper is heavily focused on GRI standards, and UN Sustainable Development Goals, it is or will be relevant or more relevant for US corporations that operate internationally. The extent, if any, to which select provisions in the paper are made applicable to US corporations and/or other organizations what operate solely or primarily domestically in the US is yet to be seen.

Best to you. David Tate, Esq.

——————————————————————–

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes, Mediator & Governance: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrationshttp://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, and risk managementhttp://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, etc.; and advising audit committees, governance committees, officers, directors, and boards.

This month (November 2020) COSO (the Committee of Sponsoring Organizations of the Treadway Commission) made available its new publication Compliance Risk Management: Applying the COSO ERM Framework which is authored by the Society of Corporate Compliance and Ethics (SCCE) and the Health Care Compliance Association (HCCA), and is the product of the SCCE & HCCA Working Group on the Application of ERM to Compliance Risk. COSO commissioned the project.

COSO is a private sector initiative that is jointly sponsored and funded by the American Accounting Association, the American Institute of CPAs, Financial Executives International, the Institute of Management Accountants, and the Institute of Internal Auditors.

In and by itself the fact of the publication does not mandate by law that the publication or any part of it must be followed or implemented by any particular organization. Of course, however, licensing or regulatory bodies could mandate the use of the publication or parts thereof, or an organization itself also could by choice decide to use and implement the publication. The publication is noteworthy for its detail and specifics, because of the reputations and followings of the authoring and commissioning organizations, and because its contents, if they are read and implemented, appear to move ERM in the context of compliance significantly forward from earlier materials. The materials are detailed (29 pages of detail and specifics, plus Appendix 1 and Appendix 2).

I wanted to make you aware of these new materials, although it will take me a while to study and discuss them in detail. The Introduction in part states “This publication aims to provide guidance on the application of the COSO ERM framework to the identification, assessment, and management of compliance risks by aligning it with the C&E program framework, creating a powerful tool that integrates the concepts underlying each of these valuable frameworks.” For the purpose of the publication the “C&E program framework” is described in Appendix 1 Elements of an Effective Compliance and Ethics Program.

The following is a link to a pdf of Compliance Risk Management: Applying the COSO ERM Framework, from the coso.org website:

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation.

Thank you for reading this post. I ask that you also pass it along to other people who would be interested as it is through collaboration that great things and success occur more quickly. And please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

Best to you, David Tate, Esq. (and inactive California CPA) – practicing in California only

Litigation, Disputes, Mediator & Governance: Business, Trust/Probate, Real Property, Governance, Elder Abuse, Investigations, Other Areas

Blogs: Trust, estate/probate, power of attorney, conservatorship, elder and dependent adult abuse, nursing home and care, disability, discrimination, personal injury, responsibilities and rights, and other related litigation, and contentious administrations http://californiaestatetrust.com

Business, D&O, board, director, audit committee, shareholder, founder, owner, and investor litigation, governance and governance committee, responsibilities and rights, compliance, investigations, and risk management http://auditcommitteeupdate.com

My law practice primarily involves the following areas and issues:

Trust, Estate, Probate Court, Elder and Dependent Adult, and Disability Disputes and Litigation

Trust and estate disputes and litigation, and contentious administrations representing fiduciaries, beneficiaries and families; elder abuse; power of attorney disputes; elder care and nursing home abuse; conservatorships; claims to real and personal property; and other related disputes and litigation.

Business, Business-Related, and Workplace Disputes and Litigation: Private, Closely Held, and Family Businesses; Public Companies; Nonprofit Entities; and Governmental Entities

Business v. business disputes including breach of contract; unlawful, unfair and fraudulent business practices; fraud, deceit and misrepresentation; unfair competition; licensing agreements, breach of the covenant of good faith and fair dealing; etc.

Misappropriation of trade secrets.

M&A disputes.

Founder, officer, director and board, investor, shareholder, creditor, VC, control, governance, decision making, fiduciary duty, conflict of interest, independence, voting, etc., disputes.

Buy-sell disputes.

Funding and share dilution disputes.

Accounting, lost profits, and royalty disputes and damages.

Insurance coverage and bad faith.

Access to corporate and business records disputes.

Employee, employer and workplace disputes and processes, discrimination, whistleblower and retaliation, harassment, defamation, etc.

Investigations, Governance, and Responsibilities and Rights

Corporate, business, nonprofit and governmental internal investigations.

Board, audit committee, governance committee, and special committee governance and processes, disputes, conflicts of interest, independence, culture, ethics, etc.; and advising audit committees, governance committees, officers, directors, and boards.

{kind=link}