I have linked below a pdf of a new California Appellate Court case (Palm Springs Villas II Homeowners Association, Inc. v. Erna Parth), discussing, under California law, whether the business judgment rule defense exists, at least for the purpose of a motion for summary judgment, when there is or might be evidence that the defendant director or officer did not satisfy duties required of her under the California statutory business judgment rule and entity governance document provisions. The decision is important for several reasons, at least including, that the decision, whether or not you agree with it, is well-written and contains good discussions about the requirements on a motion for summary judgment and other cases discussing the applicability of the California statutory business judgment rule and the related defense, and the decision should apply to both California corporate and nonprofit entities, and possibly also to California partnerships, unincorporated association entities, and religious entities.

In other words, if you are a California entity director or officer, you should read this decision, which will help to explain some of your duties and responsibilities, and that limitations might apply to your business judgment rule defense. And I should also say that it really should not come as a surprise that a California Appellate Court could hold that the business judgment rule defense might not apply in an appropriate factual situation where there might be evidence for example that a director or officer might not have sufficiently satisfied due diligence, investigation or authorization requirements prior to taking actions, even if there is no evidence of intentional wrongdoing or neglect.

Click on the following link for a pdf of the appellate decision in Palm Springs Villas II Homeowners Association, Inc. v. Parth, Palm Springs Villas v. Parth – discussing the business judgment rule defense in light of possible violations of governance documents – California law

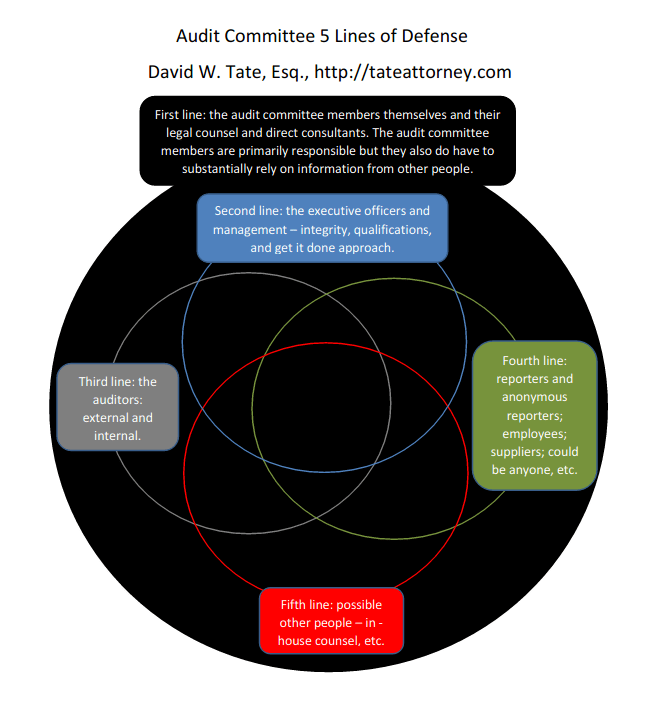

You can also see similar discussions and issues in various cases out of Delaware and under the federal securities laws. Directors and officers really need to understand and satisfy the business judgment rule in addition to other duties, and understand and satisfy the applicable provisions that are in governance documents such as by-laws, charters and CC&Rs. You will find a further discussion about the business judgment rule in my detailed Tate’s Excellent Audit Committee Guide, updated January 2016, which you can view and print if you wish from the following blog post, at no cost and without having to provide any information about yourself – click on the following link for the post containing the link to the guide CLICK HERE

Best to you, Dave Tate, Esq., San Francisco Bay Area and throughout California