I have been reading an email thread by some very good auditors and risk management professionals. It struck a chord with me. The discussion was about derivatives in general.

One participant posted recent comments or possible comments by Warren Buffett about the difficulties of evaluating derivative transactions and banks and companies that hold derivative contracts or instruments.

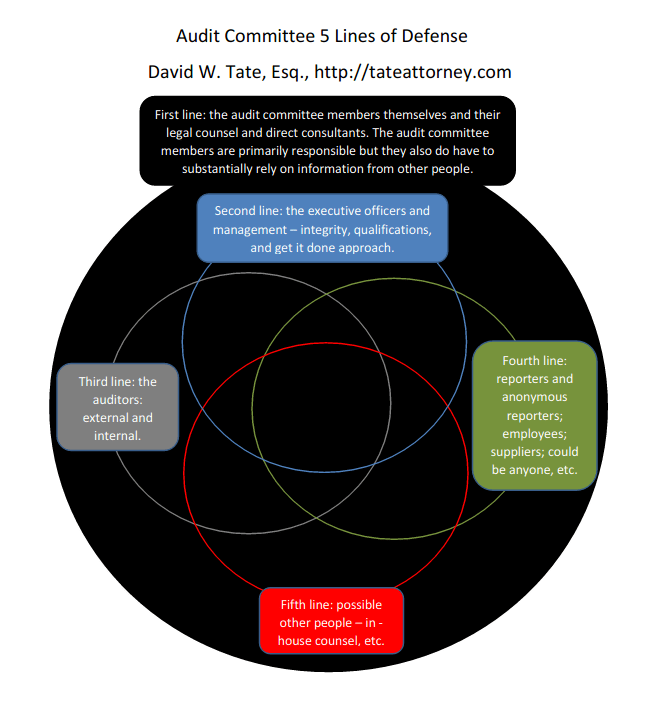

Another participant differentiated auditing and risk management in the context of derivatives – stating that the external auditor audits to determine whether the derivative transaction has been properly accounted for within the context of generally accepted accounting principles.

But the auditor’s clean opinion really doesn’t tell management, or the board, or the audit committee, or the investor how the derivative will behave or react in different situations, or the risk associated with the derivative. Of course, that audit weakness also is true with respect to all audited transactions – the auditor is only telling you that within GAAP and GAAS, and the determined level of materiality, the transactions have been properly recorded. Although proper accounting is important, the risk associated is equally and perhaps more important.

A few of my other posts have discussed derivatives – here is a link to a post about derivatives and audit committees http://wp.me/p75iWX-h.

And, as audit committees have oversight of risk management or certain aspects of risk management (which is too vague of a term (i.e., risk management), and lacking in specifics for my liking, see also http://wp.me/p75iWX-1F re risk management, audit committees, and AC charters ), as an audit committee member should you evaluate whether you and your committee, and management, are sufficiently on top of the derivative issue and the risks that they might present to your entity and its shareholders, and to you and your reputation? I’m not anti-derivative – they can be helpful and prudent – I’m simply saying that as part of your oversight and diligence you should consider whether you and your organization are sufficiently on top of the issue and understand the risks that the different derivative instruments and transactions present.

And here is a link to my audit committee guide, updated January 2016, http://wp.me/p75iWX-q

Thanks for reading. Dave Tate, Esq. (San Francisco/California)