You may have seen this month news about new SEC rules relating to the use of derivatives by registered investment companies. Related to the derivatives topic, I found a Wall Street Journal article about restatements and Commissioner Luis A. Aguilar’s December 11, 2015, speech about derivatives interesting from an audit committee perspective.

In particular, I have pasted below a snapshot from the Wall Street Journal article discussing common causes of restatements – you will note that derivatives are listed (click on the snapshot to enlarge).

Frankly, although revenue recognition is well-known as the big cause of restatement, I had not considered the importance of derivatives as a top five cause. Every public entity is different of course, however, the Wall Street Journal statistics suggest that all audit committee members, not just those of registered investment companies take into consideration the extent to which their entity is involved in derivatives and related accounting, and consider whether oversight in the derivative area is appropriate, and whether each audit committee member is sufficiently knowledgeable about derivatives and their accounting, or needs some additional continuing education.

Accounting for derivatives is complicated – I myself have pulled the derivative accounting materials off the shelf for another refresher. I have also pasted below a snapshot from some of Commissioner’s speech which I found interesting.

Immediately below is the snapshot from the Wall Street Journal article listing accounting standards or areas most commonly involved in financial restatements for the recent period 2011-2012.

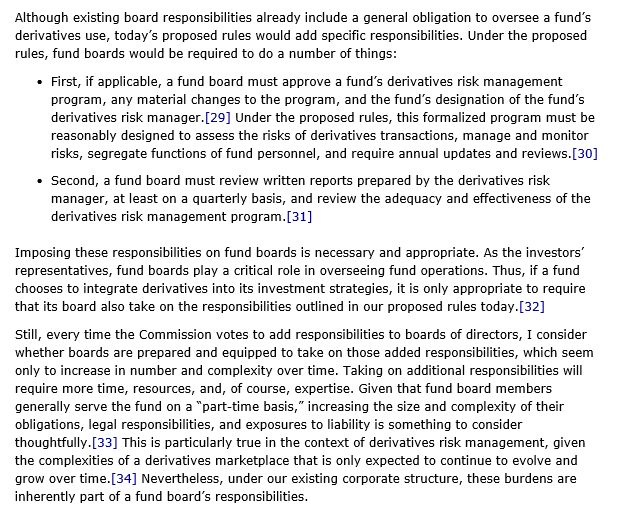

The following is a snapshot from some of SEC Commissioner Aguilar’s December 11, 2015, speech about accounting for derivatives in the context of registered investment companies.

Commissioner Aguilar also commented about the extent of the global derivatives market: “Meanwhile, the global derivatives market remains huge, at an amount estimated in excess of $630 trillion in notional value worldwide.[4]” You can see Commissioner Aguilar’s speech at:

http://www.sec.gov/news/statement/protecting-investors-through-proactive-regulation-derivatives.html

It would not surprise me if derivatives and accounting for derivatives take on greater importance for audit committee oversight in the future, for all companies that have significant derivative activities and not just for registered investment companies.

Enjoy, and onward.

Tate’s Excellent Audit Committee Guide (updated October 24, 2015, 172 pages) – click on the following link – please use and pass along to other people who would be interested – https://auditcommitteeupdate.files.wordpress.com/2015/10/tates-excellent-audit-committee-guide-10242015.pdf

Dave Tate, Esq. and California CPA (inactive), San Francisco and throughout California